Forex Trading Analysis – There was reduced liquidity in the Asian session due to the observance of the Chinese New Year festivities. However, there was still business to be attended to as the Bank of Japan re-appointed Governor Kuroda for a second term at the helm. There were also two deputy governors nominated: Amamiya is the current Bank of Japan Executive Director and Masazumi Wakatabe is a university academic. Both are quite dovish in their outlook so the current monetary policy is unlikely to change.

The subsequent move lower in USDJPY drove price under the 106.000 level to hit a low of 105.545. Japanese Finance Minister Aso made the comment that the Yen’s strength was not enough to require intervention.

ECB’s Lautenschlager spoke yesterday, making the following comments: That there might be a need for more macroprudential policy, meaning a tightening of existing borrower-based measures. The toolbox defined by the EU legal framework may be too small to address all types of systemic risk. Stability risks are not too pronounced for now.

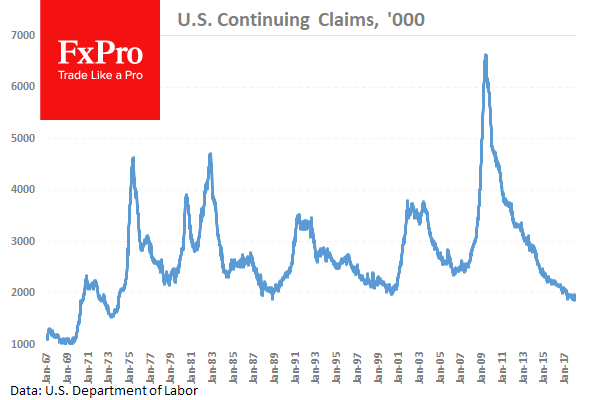

US Continuing Jobless Claims (Feb 2) were 1.942M v an expected 1.925M, from a previous number of 1.923M, which was revised up to 1.927M. Initial Jobless Claims (Feb 9) were as expected at 230K, from a prior reading of 221K, which was revised up to 223K. Philadelphia Fed Manufacturing Survey (Feb) was 25.8 v an expected 21.1, from a prior 22.2. EURUSD moved higher from 1.24619 to 1.24867 after this data release.

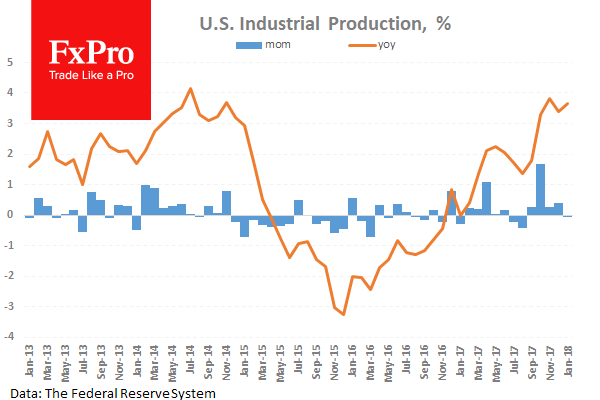

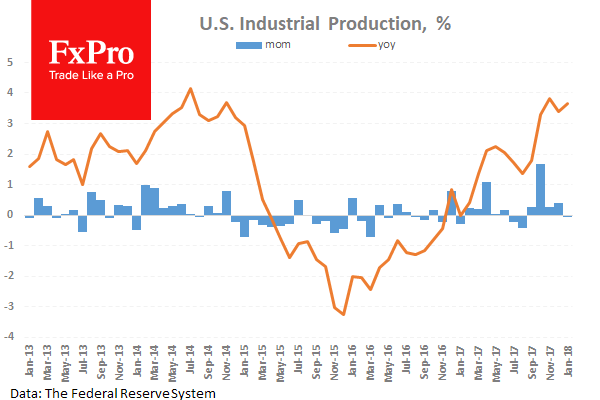

US Industrial Production (MoM) (Jan) was released coming in at -0.1%. The consensus was for 0.2%, from 0.9% previously, which was revised down to 0.4%. Capacity Utilization (Jan) was also released at this time, coming in at 77.5% with an expectation for 78.0%, from 77.9% prior, which was revised down to 77.7%.

US NAHB Housing Market Index (Feb) was released, with the value remaining unchanged, as expected, at 72. EURUSD dropped from 1.25054 to 1.24739.

Canadian BOC Governing Council Member Schembri spoke at the Manitoba Association for Business Economics in Winnipeg. Some of the comments made were: Subdued growth may change how central banks react. Higher debt levels, a decline in interest rates and decreasing economic growth could challenge policy framework.

If cyclical forces coming out of a downtrend are less powerful than historically because of demographics and debt, central banks might have to be more aggressive. BOC’s 2% target is symmetric. Negative policy rates in some jurisdictions appear to be less effective in stimulating economic growth.

New Zealand Business NZ PMI (Jan) was released coming in at 55.6. The prior number was 51.2.

Australian RBA Governor Lowe testified before the House of Representatives’ Standing Committee on Economics in Sydney. Some of the comments were: it is more likely the next interest rate move will be up. Improvement in the global economy has continued. The labour market is noticeably stronger than the RBA had expected. The strength of consumer spending remains uncertain.

There will be slow growth in household incomes for some time yet. Less monetary stimulus will be appropriate at some point. The outlook for US budget deficits is very problematic and the RBA would not want tax cuts in Australia to lead to higher deficits.

Foreign Investment in Japan stocks (Feb 9) was ¥-429.5B from a previous number of ¥-125.6B, which was revised down from ¥-126.7B. Foreign Bond Investment (Feb 9) was ¥-973.2B from a prior number of ¥-866.6B, which was revised up from ¥-864.9B. USDJPY moved down from 106.408 to 106.051 after this data was published.

EURUSD is up 0.24% overnight, trading around 1.25361.

USDJPY is down -0.37% in early session trading at around 105.731.

GBPUSD is up 0.21% to trade around 1.41292.

AUDUSD is up 0.40% overnight, trading around 0.79740.

Gold is up 0.32% in early morning trading at around $1,357.50.

WTI is up 0.07% this morning, trading around $61.35.

Major data releases for today:

At 07:00 GMT, Wholesale Price Index (MoM) (Jan) is expected to be 0.2% from -0.3% previously. Wholesale Price Index (YoY) (Jan) was 1.8% previously. EUR pairs could have positions opened or closed due to this data.

At 08:20 GMT, ECB’s Coeure will speak and this may impact on moves in EUR crosses.

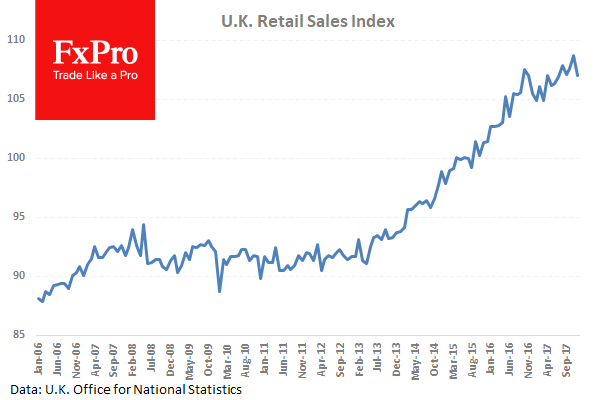

At 09:30 GMT, UK Retail Sales (YoY) (Jan) is expected to be 2.6% from 1.4% previously. Retail Sales (MoM) (Jan) is expected at 0.5% from a prior -1.5%. Retail Sales Ex-Fuel (YoY) (Jan) is expected to be 2.5% from 1.3% previously. Retail Sales Ex-Fuel (MoM) (Jan) is expected at 0.6% from a prior -1.6%. GBP crosses could experience an increase in volatility following this data release.

At 13:30 GMT, US Housing Starts (MoM) (Jan) is expected at 1.234M from a previous number of 1.192M. Building Permits (MoM) (Jan) is expected to come in at 1.300M from a prior reading of 1.302M. Housing Starts Change (Jan) is expected at 3.4% from a previous number of -8.2%. Building Permits Change (Jan) is expected to come in at 3.5% with a prior reading of -0.1%. USD crosses could see increased volatility around this data release.

At 18.00 GMT, Baker Hughes US Oil Rig Counts will be released, with a headline number from last week of 791. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

Source:Fxpro Broker

Open a real account and receive 4.25$ the Forex Cashback

Categories :

Tags : Forex Trading Analysis