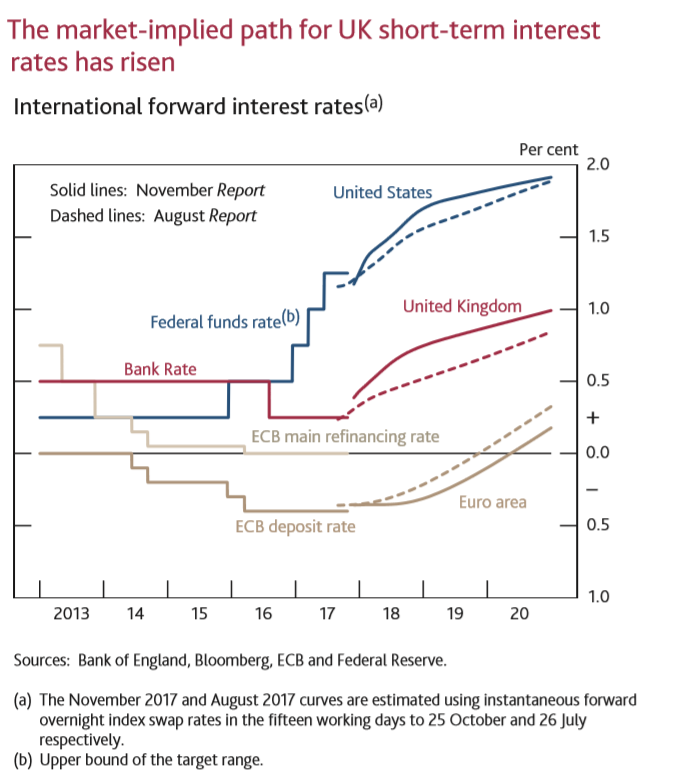

In line with market expectations, the Bank of England raised the UK base rate to 0.5% (from 0.25%) on Thursday. The rise, the first in 10 years, was widely expected as the UK has seen inflation well above the Bank of England’s target rate of 2.0% (3.0% in September), with Governor Carney stating “The pace at which the economy can grow without generating inflationary pressures has fallen relative to pre-crisis norms. This reflects persistent weakness in productivity growth since the crisis and, more recently, the more limited availability of labour.” Whilst the rate hike was already “priced-in” by the markets, GBP suffered losses of 1.8% against EUR and 1.5% against USD following the announcement. Many attribute the downward pressure on GBP because of Governor Carney hinting that rates would rise twice more in the next 3 years, with rates edging up to 1% by the end of 2020. The future pace of rate rises is exceptionally slow and it is based on a relatively gloomy growth outlook which resulted in the markets selling GBP against its peers.

To no surprise, President Trump nominated Jerome Powell as the next Federal Reserve Chairman on Thursday at the White House. Trump stated: “He’s strong, he’s committed, he’s smart” and “I am confident that with Jay as a wise steward of the Federal Reserve, it will have the leadership it needs in the years to come.” The position requires Senate confirmation, but Mr. Powell is likely to get broad support from the Republican Senate majority. The Fed is expected to raise its benchmark interest rate again in December, likely Ms. Yellen’s final act as Fed Chair. Under Mr. Powell’s leadership, the Fed will likely continue its projected path of raising its interest rate 3 more times next year, as well as continuing to pare back its massive Fixed Income portfolio.

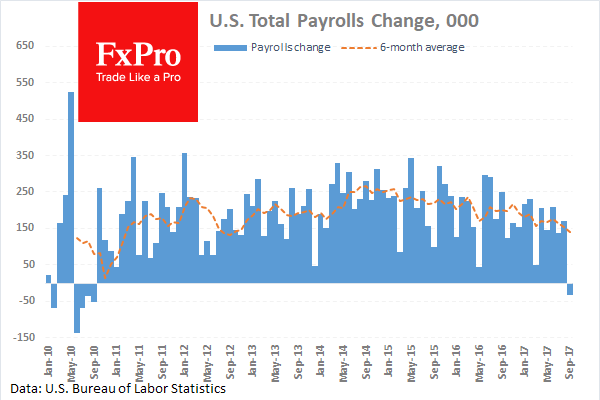

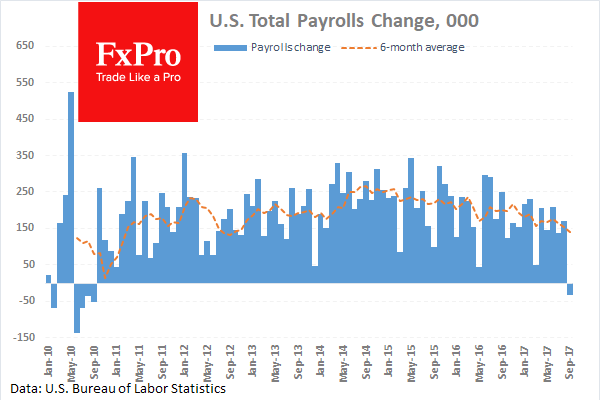

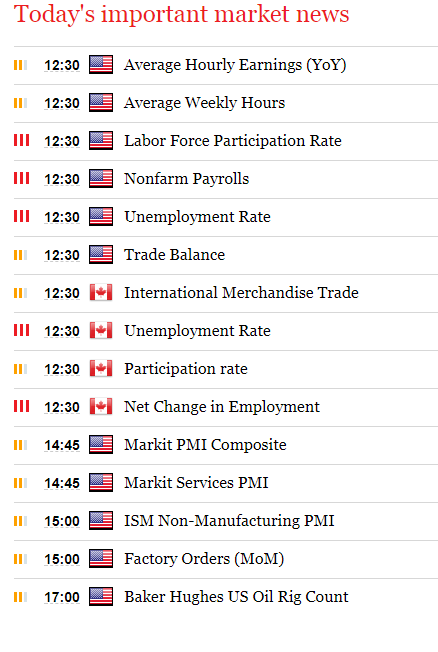

The markets are now focused on today’s Nonfarm Payrolls report for October, scheduled to be released at 12:30 GMT. Market expectations for a strong number were recently re-enforced with the ADP National Report showing the US private sector hired 235K workers in October, the most in 8 months.

EURUSD is little changed in early Friday trading at around 1.1665.

USDJPY is currently trading around 113.96.

GBPUSD, after a significant drop on Thursday, appears to be holding steady in early session trading at around 1.3075.

Gold is unchanged overnight, currently trading around $1,277.

WTI is 0.16% higher in early Friday trading at around $54.95.

Major data releases for today:

At 12:30 GMT, the US Department of Labor will release Nonfarm Payrolls for October. Market consensus is expected to show that the US economy added 310K jobs in October. In September, the economy shed jobs for the first time in 7 years, following disruptions from Hurricanes Harvey & Irma. NFP never fails to cause general market volatility, and this release will be no different, with expected volatility regardless of the number released.

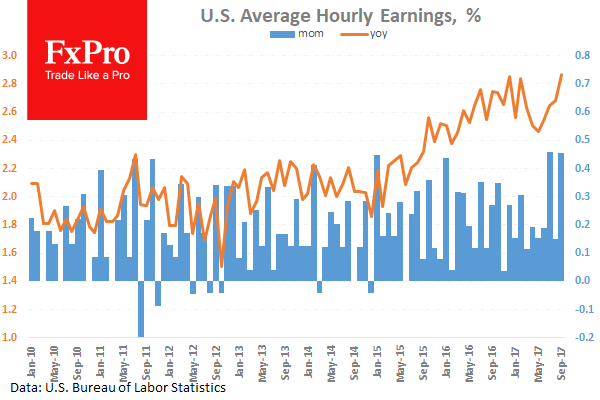

At 12:30 GMT, US average hourly earnings (MoM & YoY) for October will be released. The annualized rate rose to 2.9% in September, demonstrating the fastest pace of growth in 8 years. This pace is expected to slow down to 2.7% year-on-year in October and 0.3% month-on-month from September’s 0.5%.

At 12:30 GMT, and to round off the set of impactful data releases from the US, will be US Unemployment rate. Forecasts are calling for the rate to remain unchanged at 4.2% – any deviation from expectation will cause a spike in USD volatility.

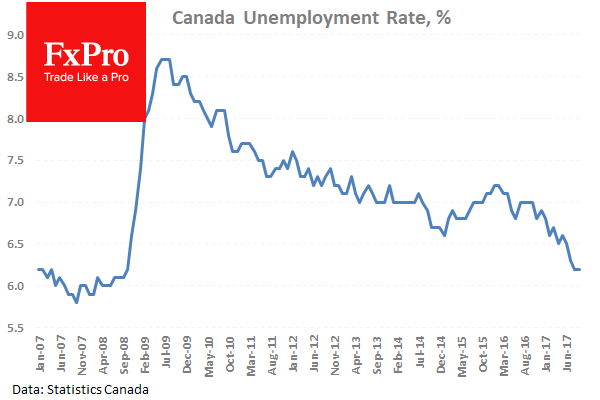

At 12:30 GMT, Statistics Canada is scheduled to release Unemployment rate and the Net Change in Employment for October. The Unemployment rate is expected to come in unchanged at 6.2%, with the net change forecast at 15K, an increase from the previous reading of 10K. Expect CAD volatility following the releases.

Source: Fxpro Forex Broker

Fxpro Forex Broker Review and Details

Categories :

Tags : Nonfarm Payrolls report US Unemployment rate